Google data science post example¶

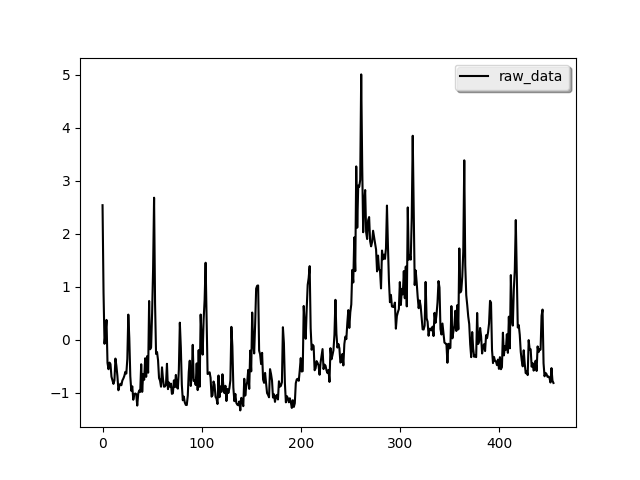

We use the example from the Google data science post to showcase pydlm. The code and data is placed under examples/unemployment_insurance/…. The data is the weekly counts of initial claims for unemployment during 2004 - 2012 and is available from the R package bsts (which is a popular R package for time series modeling). The raw data is shown below (left)

We can see strong annual pattern and some local trend from the data.

A simple model¶

Following the post, we first build a simple model with only local

linear trend and seasonality component:

from pydlm import dlm, trend, seasonality

# A linear trend

linear_trend = trend(degree=1, discount=0.95, name='linear_trend', w=10)

# A seasonality

seasonal52 = seasonality(period=52, discount=0.99, name='seasonal52', w=10)

# Build a simple dlm

simple_dlm = dlm(time_series) + linear_trend + seasonal52

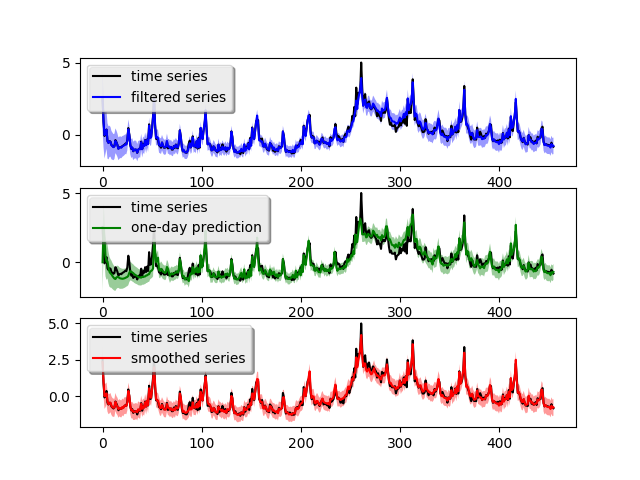

In the actual code, the time series data is scored in the variable time_series. degree=1 indicates the trend is a linear (2 stands for quadratic) and period=52 means the seasonality has a periodicy of 52. Since the seasonality is generally more stable, we set its discount factor to 0.99. For local linear trend, we use 0.95 to allow for some flexibility. w=10 is the prior guess on the variance of each component, the larger number the more uncertain. For actual meaning of these parameters, please refer to the user manual. After the model built, we can fit the model and plot the result (shown above, right figure):

# Fit the model

simple_dlm.fit()

# Plot the fitted results

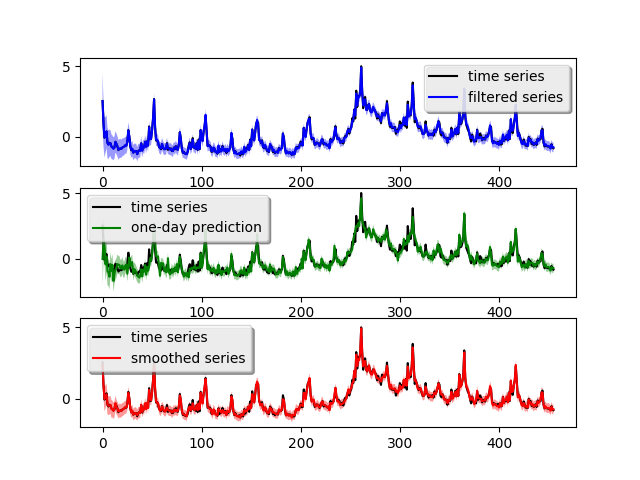

simple_dlm.turnOff('data points')

simple_dlm.plot()

The blue curve is the forward filtering result, the green curve is the one-day ahead prediction and the red curve is the backward smoothed result. The light-colored ribbon around the curve is the confidence interval (you might need to zoom-in to see it). The one-day ahead prediction shows this simple model captures the time series somewhat good but loses accuracy around the peak crisis at Week 280 (which is between year 2008 - 2009). The one-day-ahead mean squared prediction error is 0.173 which can be obtaied by calling:

simple_dlm.getMSE()

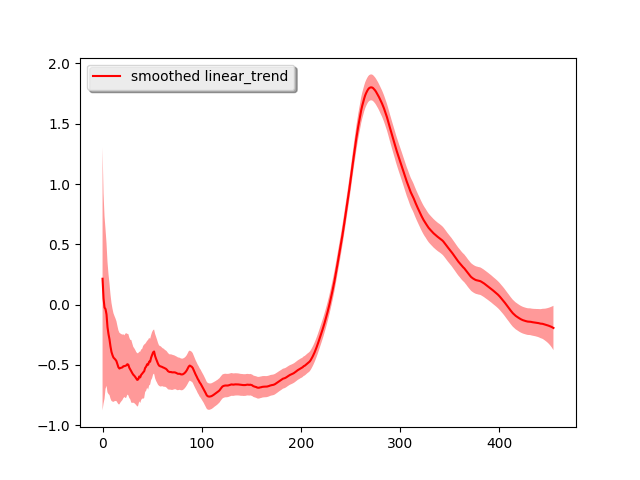

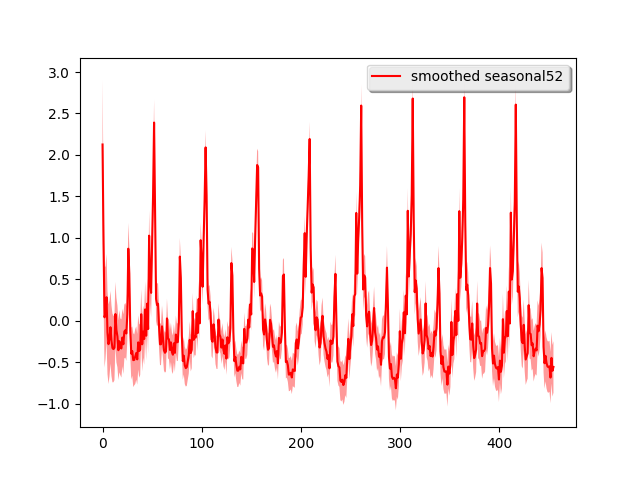

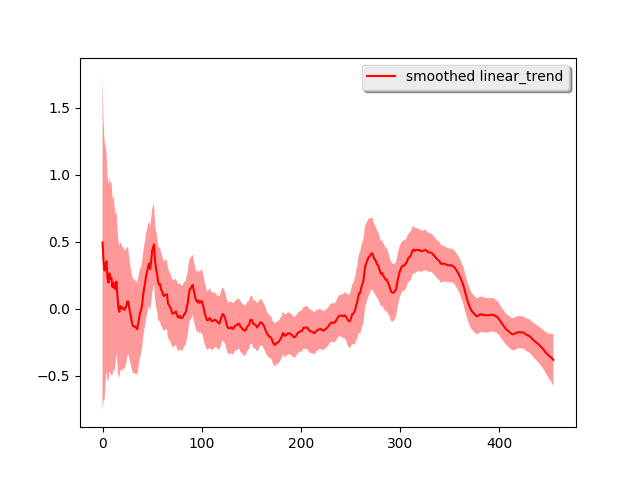

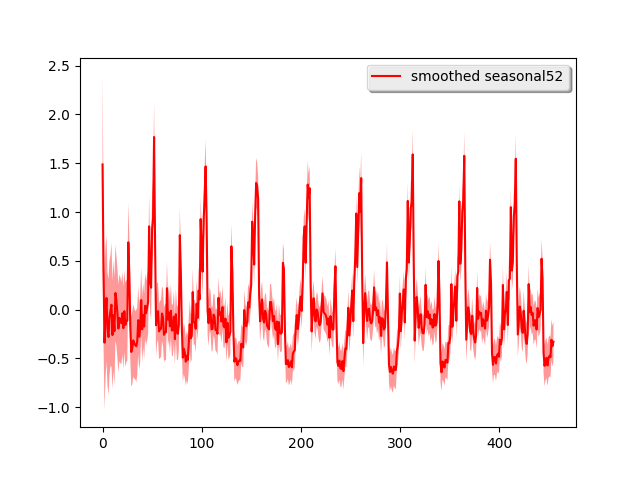

We can decompose the time series into each of its components:

# Plot each component (attribute the time series to each component)

simple_dlm.turnOff('predict plot')

simple_dlm.turnOff('filtered plot')

simple_dlm.plot('linear_trend')

simple_dlm.plot('seasonal52')

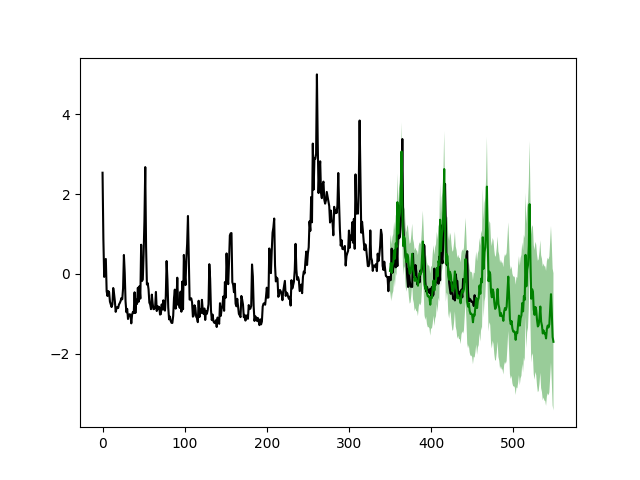

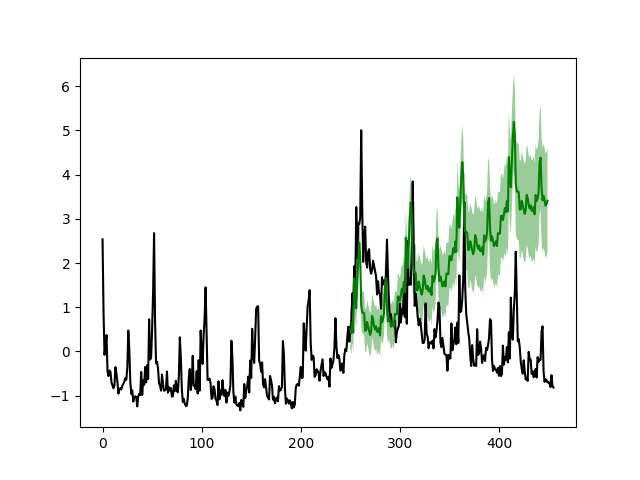

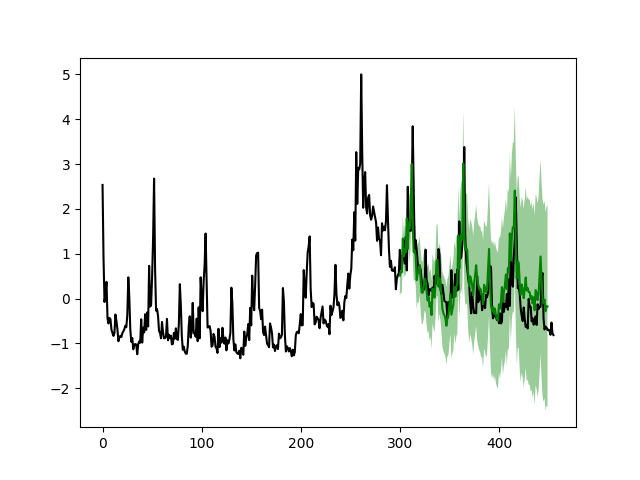

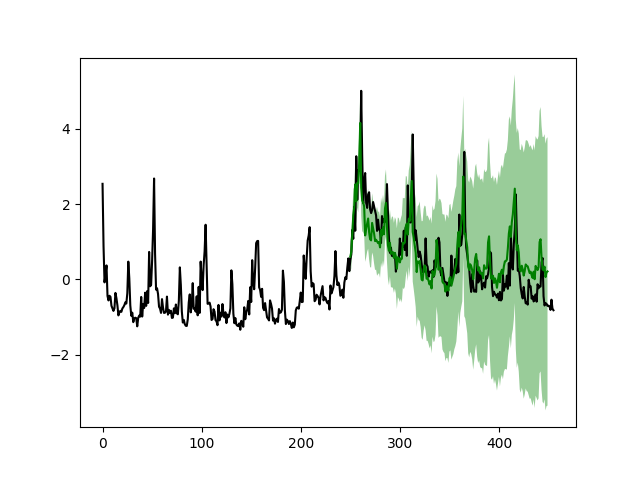

Most of the time series shape is attributed to the local linear trend and the strong seasonality pattern is easily seen. To further verify the performance, we use this simple model for long-term forecasting. In particular, we use the previous 351 week ‘s data to forecast the next 200 weeks and the previous 251 week ‘s data to forecast the next 200 weeks. We lay the predicted results on top of the real data:

# Plot the prediction give the first 351 weeks and forcast the next 200 weeks.

simple_dlm.plotPredictN(date=350, N=200)

# Plot the prediction give the first 251 weeks and forcast the next 200 weeks.

simple_dlm.plotPredictN(date=250, N=200)

From the figure we see that after the crisis peak around 2008 - 2009 (Week 280), the simple model can accurately forecast the next 200 weeks (left figure) given the first 351 weeks. However, the model fails to capture the change near the peak if the forecasting start before Week 280 (right figure).

Dynamic linear regression¶

Now we build a more sophiscated model with extra variables in the data file. The extra variables are stored in the variable features in the actual code. To build the dynamic linear regression model, we simply add a new component:

# Build a dynamic regression model

from pydlm import dynamic

regressor10 = dynamic(features=features, discount=1.0, name='regressor10', w=10)

drm = dlm(time_series) + linear_trend + seasonal52 + regressor10

drm.fit()

drm.getMSE()

# Plot the fitted results

drm.turnOff('data points')

drm.plot()

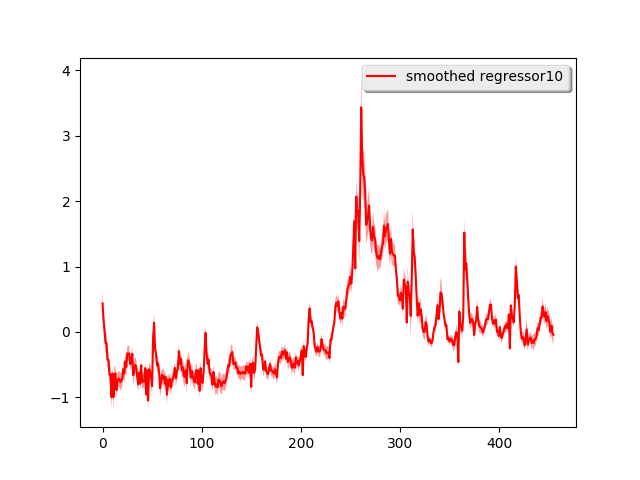

dynamic is the component for modeling dynamically changing predictors, which accepts features as its argument. The above code plots the fitted result (top left).

The one-day ahead prediction looks much better than the simple model, particularly around the crisis peak. The mean prediction error is 0.099 which is a 100% improvement over the simple model. Similarly, we also decompose the time series into the three components:

drm.turnOff('predict plot')

drm.turnOff('filtered plot')

drm.plot('linear_trend')

drm.plot('seasonal52')

drm.plot('regressor10')

This time, the shape of the time series is mostly attributed to the regressor and the linear trend looks more linear. If we do long-term forecasting again, i.e., use the previous 301 week ‘s data to forecast the next 150 weeks and the previous 251 week ‘s data to forecast the next 200 weeks:

drm.plotPredictN(date=300, N=150)

drm.plotPredictN(date=250, N=200)

The results look much better compared to the simple model